The Medishield Life Review Committee has just released the full Medishield Life Report.

For the full Medishield Life report, you can download it here:

MediShield Life Review Committee Report Final (full report)

Medishield Life at a Glance (2-page summary in 4 languages)

If you haven’t already done so, you will also want to read my Medishield Life summary.

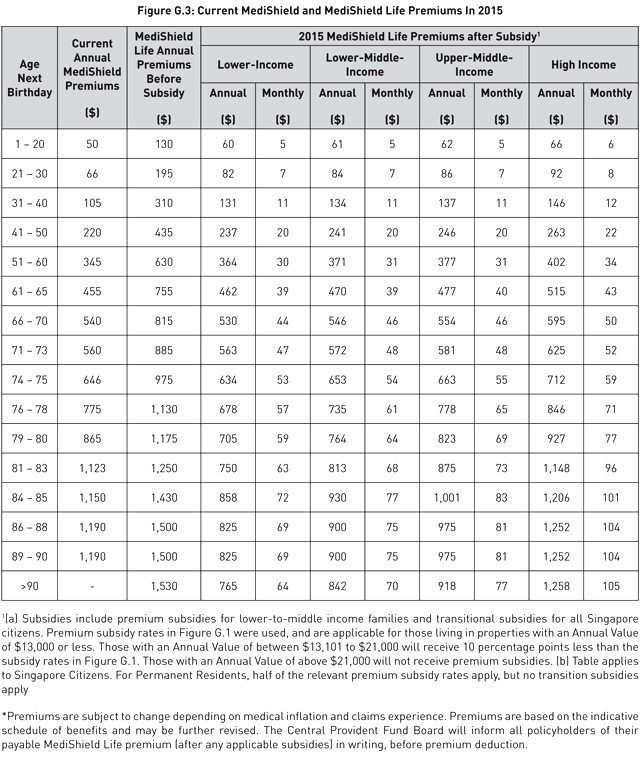

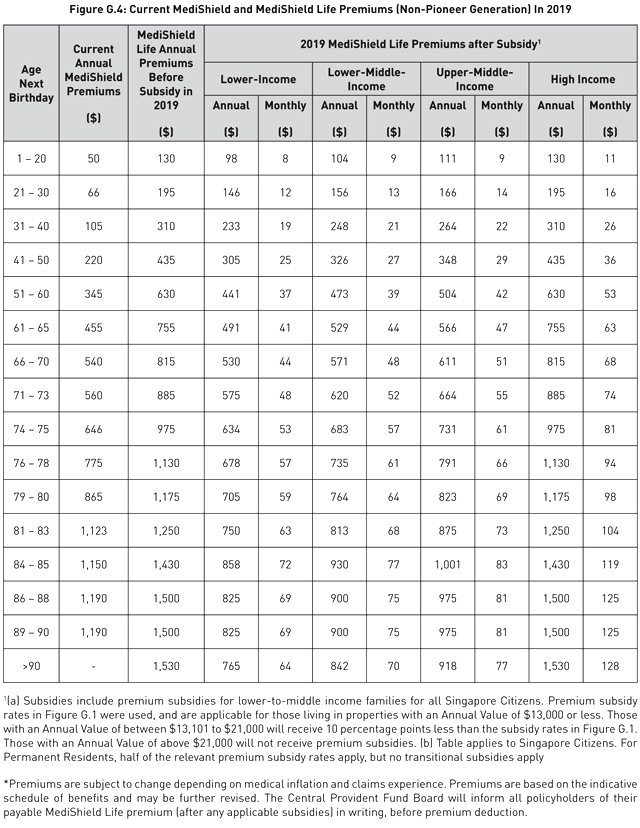

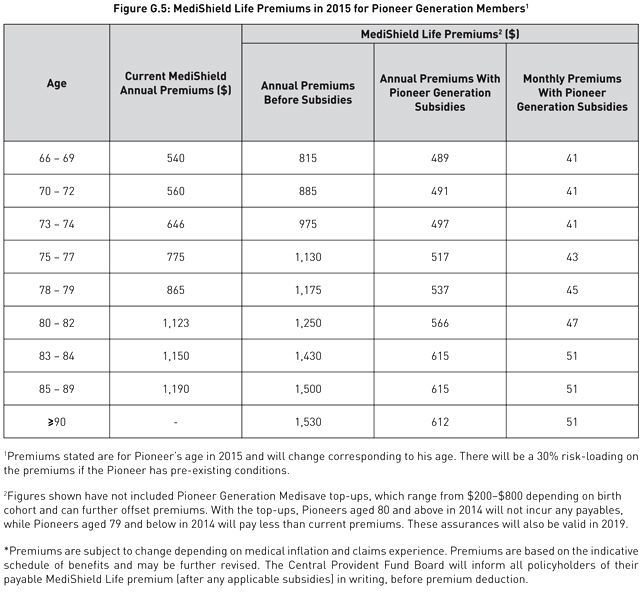

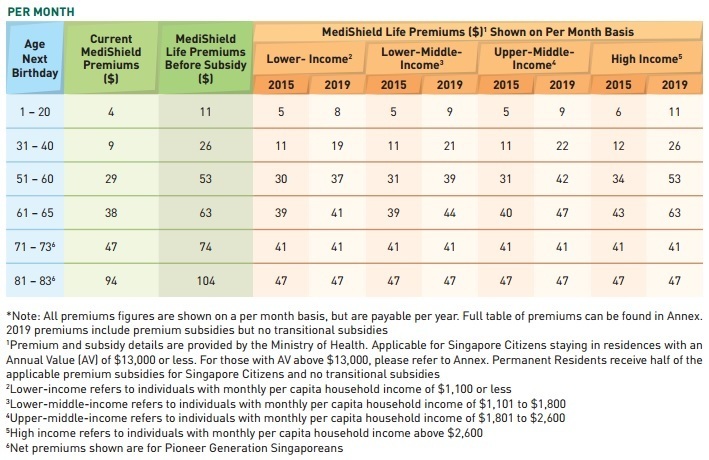

One thing that everyone has been anxious to find out is the new premiums for Medishield Life. Here’s a partial summary (full tables at the end):

There is a Medishield Life premiums calculator that can be found here: Medishield Life premiums

The bad news is that premiums are going to double or triple for the younger age groups.

The good news is that there will be temporary subsidies for everyone and permanent subsidies for the lower income.

However, everyone will feel the full burnt of the premium increases from 2019 onwards when the transitional subsidies ends.

One observation I made was that for some age bands, the new Medishield Life premiums (that is meant to provide coverage for B2 and C wards) is even higher than the current premiums for the private integrated shield plans that can coverage for B1 or even A wards (page 100 of report)!

This is very bad news for all integrated shield plan owners.

There are two reasons for this huge increase:

- Lower co-insurance for Medishield Life

- More significantly, shifting the premium cost of Medishield Life downwards towards the younger age group. See page 14 of the report, “Distributing Premiums More Evenly”.

Even then, I wonder whether the premiums are set too aggressively. With regards to this aspect, the call by the committee for more transparency on the Medishield fund is a good one (page 72).

A new recommendation that has not been announced previously is the push for government to regulate a standardized integrated shield plan that provides coverage up to B1 level (page 79). The maximium Medisave withdrawal that can be used to pay for Medishield approved plans should also be set at that level (page 80).

I think this is a good idea that will suit the needs of many Singaporeans.

The committee also spoke about the duplication with Group Employer Benefits (page 85), which is something that I wrote about previously : The Benefits of Portable Medical Plan. The committee urged employers and unions to work on this problem together.

Anyway, now that the premium values are available (see below), I will be able to finish my article on the relationship of Medishield Life with the private integrated shield plans, and what are the factors to consider in deciding whether to keep or drop the plans. Hope to get it completed sometime next week.